A parents’ love is like no other. When you see them in need, you help before it’s even asked of you. But once your children are grown up, that financial aid can begin to take its toll on your financial future.

Did you know, 79% of parents still provide financial help to their adult children? The total spending comes to $500 billion annually, while parents are saving mere $250 billion in comparison a year in their retirement accounts. All this spending and less saving is resulting a level of negligence when it comes to your own retirement savings.

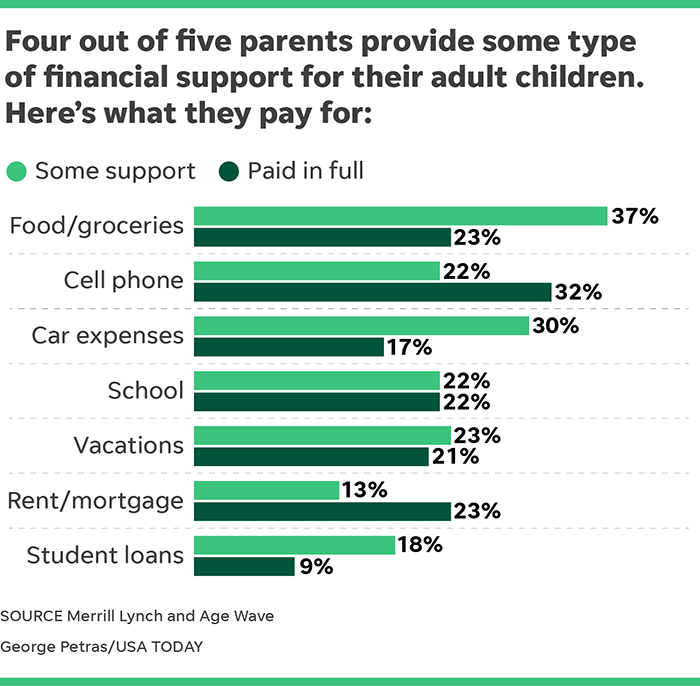

The Bank of Mom and Dad

If you’re one of the parents who is still giving money to your adult children, you’re not alone. 80% of parents of adult children are covering, or have covered, at least a portion of their adult children’s expenses after they turned 18. And while it’s important to help your kids transition to adulthood, doing so shouldn’t cripple your retirement savings. So where is this money going?

In CKS Summit Group’s previous post, we pointed out today’s young adults, ages 18 to 34, were more likely to live with their parents than were previous generations. Thirty-one percent of early adults live with their parents today, which is 50 percent higher than in 1960. Now is the time to start taking back your finances and plan for your own future.

Taking Back Control

Once children enter early adulthood, it’s about setting limits and keeping to them. There are a few steps you can take to make this process as painless and profitable as possible while still supporting your children where needed:

- Stick to a budget as best you can and understand the expenses you’re paying: Try to keep an emergency fund. And definitely continue contributing to your HSA, 401(k) or IRA.

- Have regular discussions about money: Even before children reach adulthood, also helps to instill healthy savings and budgeting habits. If you have difficulty discussing money with your adult children, consider looping in a financial advisor or other expert.

- Lend, don’t give: If your child needs money for a specific purchase, let them borrow and pay you back in affordable payments. Try automatically deducting cash from your child’s bank account, essentially acting as an interest-free loan.

- Ask for help: If your child moves back home, they should help out with the regular expenses such as utilities, groceries and rent.

- Plan ahead: If you want to help pay back student loans, contribute to your child’s wedding or give a lump sum for a down payment on a house, start planning early.

A Brighter Future

The idea of relying on your children as a financial backup when you’re older might seem appealing, but asking your adult children to help fund your retirement may put their financial security at risk.

Once children enter early adulthood, it’s about setting limits and keeping to them. Stick to a budget as best you can by understanding the expenses you’re paying. Try to keep an emergency fund. And definitely continue contributing to your HSA, 401(k) or IRA.

If you’re looking for innovative ways to make your retirement savings go the extra mile, the financial experts at CKS Summit Group boasts cutting edge tactical portfolios to help our clients achieve safe, healthy growth of their savings and preservation of their principal balance. Check out our key portfolios here, and click here to set up your complimentary strategy session today!