We may not be able to stop some financial emergencies from happening, but we can improve our ability to handle them by planning for the worst-case scenario.

Before you can safely retire, you need to know that your income will cover your expenses. But for many, surprise costs can catch retirees by surprise. All it takes is one major life-shattering event to drain your budget, and then your time of freedom and fun is over.

Understanding the key expenses that might trip you up will help you avoid these potential stumbling blocks, and ultimately help you prepare for a more comfortable and less stressful retirement.

Home Repairs/Renovations

Most Americans want to spend their golden years in their current homes, but just like us all, homes deteriorate over time. According to the HomeAdvisor’s State of Home Spending Report, American homeowners are now spending more money on home improvements than home maintenance. The average home improvement spending was at $7,560, with an average home maintenance spending at $1,105, and an average home emergency spending at $416 — for an overall total average spending of $9,081 across all categories.

To be prepared for the unexpected, you’d be smart to budget at least the total yearly amount, and consider saving additional cash in your emergency fund for larger expenses. A home equity line of credit also could come in handy.

Medical Expenses

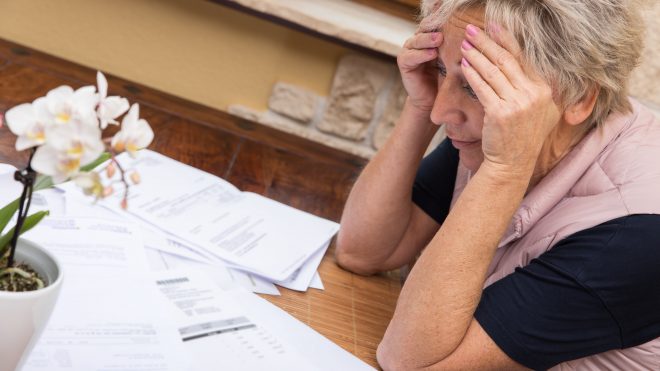

While many of us may think in general terms about the cost of health care, we often overlook just how much we will have to spend on this in retirement. A major medical expense, whether an illness or an injury from an accident, could easily cost you tens or even hundreds of thousands of dollars.

Even with Medicare coverage, seniors still incur substantial out-of-pocket costs. EBRI projects that a couple who are Medicare beneficiaries and want to be confidently prepared for the higher end of prescription drug costs would need to have $368,000 in savings to cover premiums, deductibles, and other out-of-pocket expenses. So if you think there’s a chance you may need long-term care, consider adding an insurance policy for it.

Family Members

Family can quickly become a derailing expense of your retirement funds. Especially when looking at divorce, death of a spouse or financial support to an adult child:

- Divorce: Rather than planning for joint living expenses, you might now have to divide up your savings to pay for two separate retirements.

- Death of a Spouse: Adequate life insurance to cover the funeral expenses of a spouse is also a good idea, as funeral expenses continue to rise and could put a severe dent in the fixed income of the survivor.

- Children’s Financial Support: If you have able-bodied adults relying on you for financial infusions, it may be time to close the Bank of Mom and Dad. Otherwise, financial support needs to be factored into your post-retirement budget.

Long-Term Care

Your costs for long-term care could be catastrophic, nonexistent or somewhere between. With people living longer, it’s not crazy to think that you could enter retirement with parents who are still alive.

The good news? A recent Vanguard study estimated about half of the elderly won’t have to pay for long-term care. This group either won’t need help or will have unpaid caregivers such as a spouse or adult child. The bad news? Another quarter can expect to incur costs of less than $100,000, while 15% can expect to pay more than $250,000.

Long-term care insurance may be one solution if you can get it and afford it. Otherwise, consider keeping some money in reserve. If absolutely needed, retirees could earmark some of their investments or their home equity for this purpose.

Final Thoughts

The above four life events can combine to ruin your existing retirement plans. While there’s some preparations you can make to mitigate their effects, if you are caught off guard, there are still ways to salvage enjoyment and financial comfort in your retirement years.

In 2020, all retirees should consider their potential risks and have a plan to deal with unexpected expenses. At CKS Summit Group, we believe the earlier you start planning, the more choice and control you will have. If your retirement plan isn’t equipped to deal with one or all of them, contact us here today to make adjustments now before it’s too late.